TABLE OF CONTENTS

What is an asset?

Assets are anything with economic value owned or controlled by a firm or individual. Their resale value is expected to flow directly or indirectly to the owners when sold.

Acquiring assets should allow you to increase production directly or indirectly. Your sales and revenue must also increase within their useful life.

Tip: Useful life is the tenure during which the asset is profitable to the business.

Assets can be segregated into fixed, current, liquid, tangible, intangible, fictitious, and wasting classifications.

In the IT landscape, they are primarily classified as hardware and software.

What are hardware assets?

Hardware IT assets are physical items classified as assets due to their data, financial, and mobility responsibilities. They can be grouped into laptops, computers, servers, monitors, tablets, smartphones, etc.

Hardware has a unique serial number and is assigned to a unique workstation.

You can add hardware like displays, stationery, PCs, docks, headsets, and more to a workstation.

What are software assets?

Software assets are the digital or intangible assets of an organization.

Software assets include applications for which licenses are usually issued per user or machine. They also entail systems and databases built using open-source resources. Software assets comprise cloud-based and cloud services, such as software-as-a-service (SaaS) applications.

What is depreciation?

It is an accounting method used to allocate the cost of a tangible asset over its useful life. This concept helps businesses spread out the expense over the periods it is used rather than charging the full cost to the period in which the asset was purchased.

It is the wear-and-tear cost associated with an asset.

For instance, the PC you are using to manage your business has an initial cost associated with it.

You can save a certain amount yearly from the revenue you generate with its aid. When the PC finally tears off, you have a set-aside amount to buy a new PC.

Thus, you can save amounts each year and replace the new asset.

As per John Felix Odhimbo, a blogger on LinkedIn, “Businesses residing in the US will also have to calculate depreciation based on the U.S. Tax Code, which allows businesses to take advantage of accelerated depreciation as specified by the Modified Accelerated Cost Recovery System (MACRS) rules. Accelerating the "expense" of a depreciable asset, enterprises can reduce income taxes in the early years of an asset's useful life.”

Factors to consider in depreciation

The main factors to consider in depreciation are cost, useful life, salvage value, and depreciation methods.

-

Cost of the asset: The cost principle is heavily associated with depreciation. It implies that accounting data is based on price (the cash paid or its equivalent). For example, if the market value of an asset is $5,000, but it is acquired at $4000, its recorded cost will be $4000.

-

Useful life: Refers to when an asset is functional with minor repairs to generate revenue. To find an asset's useful life, start with its physical value, any modifications, and signs of obsolescence. Also, consider the history of similar assets. An asset's economic life is shorter than its physical life. Physical life is primarily dependent on maintenance, repairs, and the intensity of use, while economic life depends on the assessment of obsolescence or technological change.

-

Salvage value: It is the scrap value of the asset. It is calculated at the end of its useful life and is equivalent to deducting disposal costs from the sale value of the investment.

-

Depreciation methods: It is calculated in five ways (we will discuss them later in the blog):. are straight line, units of production, declining balance, double declining balance, and sum of years digits.

-

Legal or regulatory requirements: Depreciation of assets is subject to the region. The legal regulation:

1. In the US, it's a Modified Accelerated Cost Recovery System (MACRS).

2. In the European Union, it's International Financial Reporting Standards (IFRS).

3. In the UK, it's the UK Generally Accepted Accounting Principles (UK GAAP).

4. In Canada, it's Canadian Generally Accepted Accounting Principles (Canadian GAAP).

Importance of depreciation

It isn't only significant in calculating the scrap value of the assets. Depreciation is an integral part of the accounting team to chalk out key metrics like:

-

Calculating profit or loss: To determine profit or loss, all expenses and revenue streams must be calculated alike. If a company does not state the depreciation costs, assets will be overvalued, causing the company's true economic value to go haywire.

-

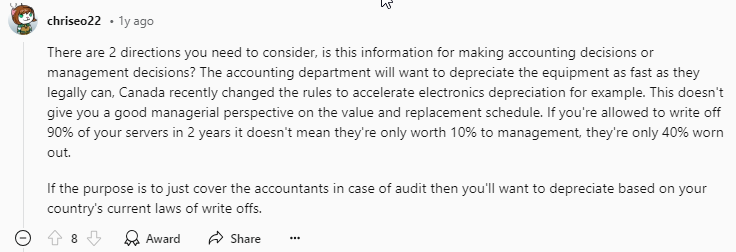

Tax benefits: Depreciation reduces the gross tax to be paid. The overall value of assets is mitigated before taxable income is calculated, lowering the taxable amount. Since depreciation is recorded as a cost to the company, it is deducted from net revenue. As per Redditor chriseo22:

-

Determining the actual cost of production: Each asset is depreciated as it is used. Thus, the actual cost of production is calculated only after adding the depreciated amount.

-

Replacement of assets: Since depreciation costs are spent along with production, they are non-cash expenses. This amount is not paid in terms of cash and is thus used to replace assets after their useful life.

-

Affecting business value: As the assets lose value over time, not registering them can overestimate your revenue, which can set false expectations for financial future planning.

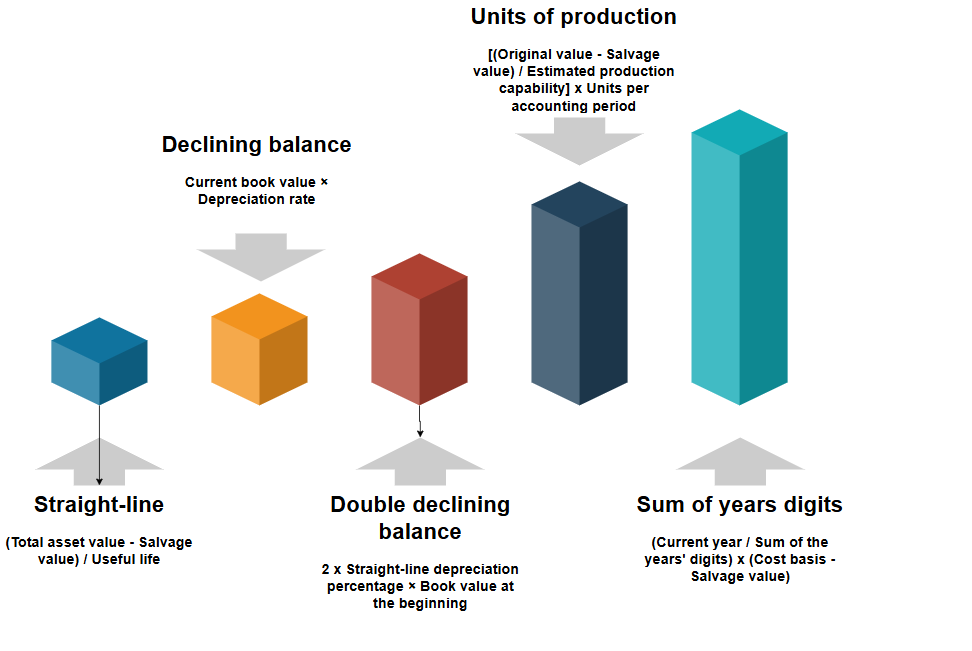

Types of methods to calculate depreciation

The depreciation of your IT assets heavily relies on the structure your company follows.

There are different types of depreciation, and the formula for implementation can vary based on factors such as taxes, equipment costs, and usage.

(Made via draw.io)

Straight-line

The most convenient and easy method of hardware asset depreciation is straight-line.

You can easily set it up in your asset management database, ITSM, or the most popular ITAM tool, i.e., Microsoft Excel.

Straight-line = (Total asset value - Salvage value) / Useful life

*Salvage value: It is the estimated book value of an asset after depreciation

Ideal situation: You can use the straight-line method if your organization doesn't have an accountant or tax advisor. Also, choose to go by the straight line if the value of your asset diminishes constantly year over year.

An example of the straight-line method: For example, if a piece of equipment has a total asset cost of $5,000, an estimated useful life of 5 years, and a salvage value of $1000, the annual expense would be calculated as follows:

SLD = (5000 - 1000) / 5

Thus, the straight-line expense is 800.

Pros of straight-line calculation

-

Save on taxes: The straight-line method can significantly reduce your taxes since your IT assets are continuously depreciating. This implies that your taxable income decreases consistently yearly as the asset depreciates.

-

Forecasting: Your financial forecasting becomes more reliable. As your IT asset depreciates at the same rate yearly, you can make informed decisions that positively impact your ROI.

-

Integrity and transparency: By studying the pattern in hindsight, even your new members can understand financial statements. They can gauge how much more will be lost in the future and what assets will be appreciated.

Cons of straight-line calculation:

-

Aging factor: You may miss an asset's growing factor. It is noteworthy that the depreciation value of the investment might not be the same over different periods of time; however, you just ignore that probability.

-

Ignoring asset usage: You may miss the fact that the value of a depreciating asset depends on its actual usage. It might be erratic instead of following a linear pattern. However, in the straight-line method, it is assumed that the asset depreciates linearly.

-

Technology update: Due to the disruption of newer technologies, an asset may depreciate quite faster than its estimated lifetime.

If an employer has purchased assets and has been tracking them via the Workwize dashboard, they also get a bird's-eye view of how these IT assets are being depreciated. Workwize follows the linear or straight-line method until the duration they set the duration for.

Declining balance

You can calculate the accelerated value of depreciation in the former years.

Declining balance = Current book value × Depreciation rate

Ideal situation: It is appropriate for resources that require more repairs and maintenance, like computers, in the later years of their lives.

An example of a declining balance method: A computer is bought for $100,000, and the depreciation rate is 20%.

Year 1: 100000 × 20 % = $20000

Year 2: (100000 - 20000) × 20 % = $16000

Year 3: (100000 - 20000 - 16000) × 20 % = $12800

Year 4: (100000 - 20000 -16000 - 12800) X 20% = $10240

Year 5: (100000 - 20000 -16000 - 12800 - 10240) x 20% = $8192

Pros of declining balance

-

GAAP-compliant: Under GAAP (Generally Acceptable Accounting Principles), companies should use a depreciation method that accurately reflects an asset's economic value.

-

Cost-effective: Since most of the value is extracted from the asset in former years, it can help lower expenses later.

-

Tax reduction: The taxable income decreases due to more significant wear and tear in the initial years, leading to lower taxes.

Cons of declining balance

-

Inaccurate assessment: An asset's value can be overestimated or underestimated. This happens when the depreciation rate is not adjusted to match its exact usage.

-

Complex calculation: In organizations of large sizes, managing multiple assets can become cumbersome. The formula is complex, so calculating the actual depreciation value can lead to financial fallout.

-

Rigidity: The rate of depreciation is fixed and does not succumb to changes easily.

-

Inaccuracy in reporting: If the declining balance technique is not used correctly, it may result in erroneous reporting, impacting financial statements, tax filings, and other significant papers.

Double declining balance

It enables you to write off more of an asset's value in the days you immediately buy it. Compared to a declining balance, it depreciates assets twice as fast and defers income tax to later years.

Double declining balance = 2 x Straight-line depreciation percentage × Book value at the beginning

Ideal situation: It is ideal for situations where assets depreciate rapidly and become obsolete. These comprise computers, smartphones, and other gadgets that are replaced by newer technology.

An example of the double declining balance method: A smartphone is purchased for $2,000 and is to be depreciated over five years.

Double declining expense = 2 * $20,00/5 years = $8,00 per year

Pros of double declining balance

-

Writing off taxes: Scrapped assets quickly allow for a tax-deductible structure and write-off taxes to later years.

-

Recovering purchase costs: The cost spent on the asset is recovered in the initial years of purchase, thus restoring its actual value.

Cons of double declining balance

-

Hiring accountants: Calculating DDB is quite complex, so you should consider hiring an accountant to avoid costly mistakes.

-

Fixture of cost: As the money is spent on assets upfront, any financial emergency after purchase would be hard to combat.

Note: Based on the jurisdiction (U.S., Canada, U.K., etc.), you can choose the depreciation method. For instance, if you're based in the U.S., you have to use MACRS, which is DDB at the beginning of the class life of the asset and then switches to straight-line later in the asset's life.

Units of production

You can calculate an asset's depreciation value based on the units it produces instead of its useful years.

Units of production = [(Original value - Salvage value) / Estimated production capability] x Units per accounting period

Ideal situation: Use when the assets are used extensively for each delivered unit, leading to more significant wear and tear. You can focus on the number of units produced, irrespective of the number of years they've been used. It should not be used where there is no significant difference in asset usage annually.

An example of the units of production method:

Pros of units of production

-

Accuracy: You can determine the age of assets more accurately.

-

Greater value: Since these assets are used far more often, their depreciation value is higher.

-

Tax deduction: With more significant depreciation in productive years, you can offset higher costs and increase revenue.

-

Tracking profit and loss: You can track your gain and loss more accurately than other depreciation methods.

-

Higher value: You can depreciate an asset when it has delivered its full capacity or has recovered its total cost, whichever is higher.

Cons of units of production

-

Improper evaluation: This method only allows you to calculate the depreciation value. However, the asset value may lessen due to other factors.

-

Scattered assets: Tracing each asset becomes cumbersome if your company assembles several parts to make a product.

-

Inappropriate for taxation: Using this depreciation is not advisable for tax purposes.

-

Manufacturing: This method is most suitable and is only used in the manufacturing process. Other depreciation calculators are used for different purposes.

-

Time-agnostic: This method does not consider time and thus may result in inaccurate results.

Sum of years digits

It is an accelerated depreciation method in which the asset is allocated a larger percentage of its depreciation in its initial years than later.

Sum of years digits = (Current year / Sum of the years' digits) x (Cost basis - Salvage value)

Ideal situation: It is suitable for scenarios where your assets use a higher percentage of their value in the initial years.

An example of the sum of years digits is a machine valued at $50,000, with a salvage value of $2,000 and a useful life of 4 years.

4 years of useful life = 4+3+2+1

Sum of the years = 10

Depreciable base = 50,000 – 2,000 = Rs 48,000

1st year = 48000 * 4/10 = Rs.19,200

2nd year = 48000 * 3/10 = Rs.14,400

3rd year = 48000 * 2/10 = Rs.9,600

4th year = 48000 * 1/10 = Rs.4,800

Pros of sum of years digits

-

Greater revenue: This method assumes that an asset depreciates more in its earlier useful years. It is found to be more practical since the asset was more productive in its former years.

-

Repairing and maintenance: The depreciation charge is higher in the initial years, and maintenance costs are lower during this phase. As the asset ages, its depreciation costs lessen; however, repair and maintenance costs increase.

-

Stoic earnings: By adhering to the equilibrium between depreciation and maintenance, earnings are unaffected.

-

Taxation: During the initial years, tax is low since depreciation is higher.

Cons of the sum of years digits

-

Quicker depreciation: It requires keeping track of each year's depreciation fraction, which can be more time-consuming and prone to errors.

-

Lower tax liability: In later years, the lower depreciation expenses result in higher taxable income, leading to increased tax liabilities.

Workwize has IT asset management and IT asset depreciation woven into one platform

Workwize is a zero-touch platform for IT managers to automate the management of their IT hardware, no matter where it is located. It has one centralized dashboard and five features.

Here’s an overview:

-

IT Hardware Management: Overview of rented/bought or employee-owned assets, along with their current and depreciating value. The best part? Employees can access self-service IT support to request items, request repairs/ maintenance, or request any other support.

-

IT Hardware Deployment: Reliable tracking and status updates through a track-and-trace link. Out-of-the-box configured device image/enrolment into MDM, and automatic onboarding via your preferred HIRS platform.

-

IT Hardware Procurement: Global delivery of IT equipment (like laptops and IT peripherals) within days—be it warehouses, remote offices, or employees worldwide.

-

IT Hardware Retrieval: Zero-touch retrieval (communication with the employee, packaging, and logistics are handled by the logistics team), offboarding tracking, and warehousing: storage, wiping, cleaning, and redeploying. Multi-channel retrieval using email, phone, and WhatsApp.

-

IT Hardware Disposal: Get fair market value for disposed of IT hardware via our local warehouses or donate—all with a certificate of data destruction. Eco-friendly disposal processes as per the country’s regulations.

Book a Workwize Demo today and see how we can help you automate your global IT hardware management :)